Navigating the world of loans can be overwhelming, especially with so many options available. Understanding the different types of loans and their features is crucial for making informed financial decisions. This guide provides an overview of various loan types, their benefits, and considerations.

1. Personal Loans

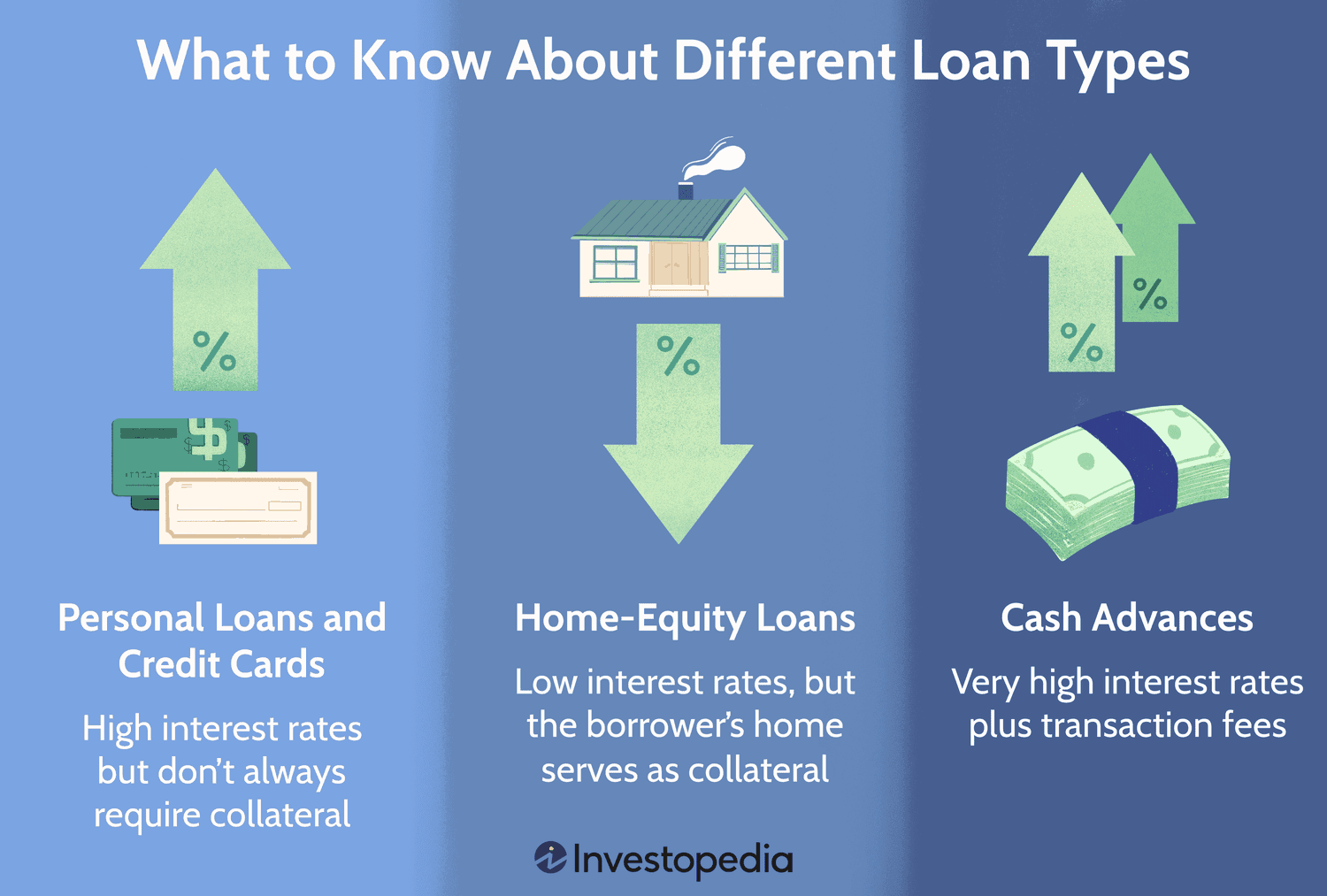

Personal loans are a versatile option for borrowers looking to finance a range of needs, such as debt consolidation, home improvements, or medical expenses.

- Key Features: These loans are usually unsecured, meaning they do not require collateral. The loan amounts and interest rates vary based on the borrower’s credit score and income.

- Interest Rates: They can be fixed or variable. Fixed rates offer stable monthly payments, while variable rates may fluctuate over time.

- Repayment Terms: Typically range from one to seven years, depending on the lender.

- Considerations: Personal loans may have higher interest rates for borrowers with lower credit scores. Additionally, borrowers should be aware of any origination fees or prepayment penalties.

2. Mortgage Loans

Mortgage loans are designed specifically for purchasing real estate. They usually have longer terms and lower interest rates compared to other loan types.

- Key Features: These loans are secured by the property being purchased. If the borrower defaults, the lender can foreclose on the property.

- Types of Mortgages: Common types include fixed-rate mortgages, adjustable-rate mortgages (ARMs), and government-backed loans like FHA, VA, and USDA loans.

- Interest Rates: Fixed-rate mortgages have a consistent rate throughout the term, while ARMs have rates that can change after an initial fixed period.

- Considerations: Mortgages require a down payment, usually between 3% to 20% of the property price. Borrowers should also consider closing costs, property taxes, and insurance.

3. Auto Loans

Auto loans are used specifically for purchasing vehicles, whether new or used. They are typically secured by the vehicle itself.

- Key Features: These loans come with fixed interest rates and terms that generally range from three to seven years.

- Interest Rates: Depend on the borrower’s credit score, loan term, and the vehicle’s age. New car loans usually have lower rates than used car loans.

- Repayment Terms: Choosing a shorter term can mean higher monthly payments but less interest paid overall.

- Considerations: Auto loans require full-coverage insurance, and missing payments can result in the vehicle being repossessed.

4. Student Loans

Student loans help cover the cost of higher education, including tuition, books, and living expenses. They can be either federal or private.

- Key Features: Federal student loans are backed by the government and often offer flexible repayment plans and lower interest rates. Private student loans are provided by banks and other lenders and may have higher rates.

- Interest Rates: Federal loans generally have fixed rates, while private loans can have fixed or variable rates.

- Repayment Terms: Federal loans often provide grace periods and income-driven repayment plans, while private loans usually have stricter terms.

- Considerations: Borrowers should exhaust federal loan options before considering private loans due to their favorable terms and protections.

5. Home Equity Loans and Lines of Credit (HELOCs)

Home equity loans and HELOCs allow homeowners to borrow against the equity in their homes. They are often used for home renovations, debt consolidation, or major purchases.

- Key Features: Home equity loans provide a lump sum with a fixed interest rate, while HELOCs offer a revolving credit line with variable rates.

- Interest Rates: Typically lower than personal loans since they are secured by the home.

- Repayment Terms: Home equity loans have fixed terms, while HELOCs offer a draw period (usually 10 years) followed by a repayment period.

- Considerations: Failure to repay can result in losing the home. Borrowers should consider the risk before leveraging home equity.

6. Small Business Loans

Small business loans provide funding for entrepreneurs to start or expand their businesses. These loans come in various forms, such as term loans, SBA loans, and business lines of credit.

- Key Features: Business loans may require collateral or a personal guarantee. The terms vary based on the loan type and lender.

- Interest Rates: Rates depend on the business’s credit profile, loan amount, and repayment term.

- Repayment Terms: Can range from a few months to several years.

- Considerations: Business owners should have a solid business plan and financial projections when applying for a loan.

7. Payday Loans

Payday loans are short-term, high-interest loans meant to cover immediate cash needs until the borrower’s next paycheck.

- Key Features: These loans are usually for small amounts and come with extremely high interest rates.

- Interest Rates: Often exceed 300% APR, making them one of the most expensive types of loans.

- Repayment Terms: Generally due in full on the borrower’s next payday, typically within two weeks.

- Considerations: Payday loans can lead to a cycle of debt due to their high costs. They should be used as a last resort.

8. Debt Consolidation Loans

Debt consolidation loans combine multiple debts into a single loan, simplifying repayment and potentially lowering interest rates.

- Key Features: These are often personal loans or home equity loans, used to pay off credit card balances, medical bills, or other high-interest debts.

- Interest Rates: Usually lower than the average credit card APR, but rates vary based on creditworthiness.

- Repayment Terms: Can range from two to seven years.

- Considerations: Borrowers should ensure they do not accumulate new debt after consolidation to avoid falling back into financial trouble.

Conclusion

Understanding the different types of loans helps borrowers make informed choices based on their needs and financial situation. Whether it’s a personal loan, mortgage, or student loan, evaluating the terms, interest rates, and repayment plans is essential for effective financial management.